28 April 2026

Can you afford to be underinsured?

3 minutes

For most of us, our home is the most valuable investment we will make in our lifetime, and insurance is critical to protecting that investment. But it needs to be correctly valued, especially as we enter the busy summer season of travelling, enjoying the outdoors and generally spending more time outside the home.

Now is the perfect time to ask: is your home insurance ready to cover it all? And is a contents policy enough, or do you need to think about a more specific policy or speak with an expert who can help you decide.

What is underinsurance?

If you had to repurchase everything in your home or rebuild the entire structure from the ground up, what’s the total value? If you’ve not got adequate cover for the full cost of repairs and replacements, you could have your claim denied or policy voided and have to pay the extra costs. Recent data shows about 76% of buildings are underinsured, leaving them incredibly exposed. So, is your cover up to scratch?

Home insurance can come in three forms: contents insurance to cover the items inside, buildings insurance to cover the build itself, or cover that combines both. Each type is designed to provide you protection in case of unexpected and potentially costly situations.

If disaster struck, would your insurance fully cover the costs? Repair costs can reach into hundreds of thousands of pounds, and if your insurance denies your claim, you are unlikely to be able to restore your home as you hoped. Underinsurance is especially worrying because of the ‘average clause’, which refers to how insurers calculate claims and decide what your payout will be if you’re underinsured. When the amount you’re insured by is less than the actual value of the property, insurers may reduce the claim payout proportionally.

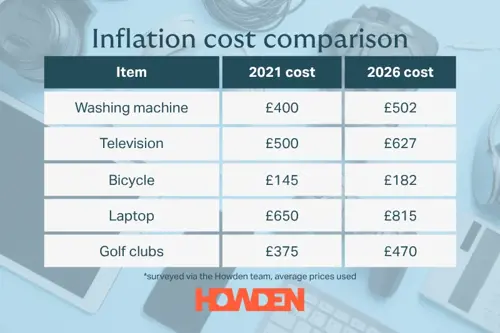

How has inflation affected your rebuild costs?

With inflation driving up prices for building materials and home furnishings, your policy may not be keeping pace with the true value of what you’d need to replace. RebuildCostASSESSMENT’s review of 2025 revealed that, based on national indices, average rebuild costs are now around 3–5% higher than the year before.

The exact figure varies significantly by region, property type, and the nature of the work involved. And while general construction inflation has eased from peaks in 2021-22, essential components, such as plumbing and kitchen installations, are increasing by around 6-8% in some cases.

It’s not just the cost of materials either. Skilled trades are still in short supply, including electricians and plumbers. When labour is harder to secure, building work can take longer and cost more, which can push up rebuild and repair prices.

Is contents insurance enough or do you need extra cover?

Rising costs don’t just affect your building. They affect what’s inside it too. From everyday appliances to valuables you’ve owned for years, replacement costs have crept up, quietly leaving your contents cover lagging behind.

Contents insurance covers the possessions inside your home. That’s typically anything you’d take with you if you moved house, including furniture, appliances, soft furnishings, gadgets and valuables. Most policies cover events like theft, fire and flooding, but not everyday mishaps. If you drop your phone or damage a laptop, you’ll likely need to add accidental damage cover to be properly protected.

It’s also worth thinking about where your belongings are used. From gadgets and sports equipment to musical instruments and jewellery, many valuable items don’t stay at home. While contents insurance may cover them indoors, protection can be limited, or stop altogether, once they’re taken out and about.

Policy limits matter too, especially for high value items. Most contents policies include a single item limit; the maximum your insurer will pay for any one item unless it’s listed separately. If something is worth more than that limit, you may not receive enough to replace it in full. For example, if your policy has a £1,500 single item limit and a £2,500 gadget is stolen, your payout may be capped unless the item was specified.

And inflation makes this even more important. With gold and silver prices at record highs, many jewellery items are now worth far more than when they were bought or last valued. Pieces that once sat comfortably within policy limits, including inherited or long-owned items, may now exceed them, leaving you underinsured without realising.

So, is contents insurance enough? Often yes, but only if it reflects what you actually own today, how you use it, and what it would really cost to replace. Reviewing values, listing high value items separately, and adding the right extensions can make all the difference. Because when something goes wrong, the last thing you want is to discover that your cover hasn’t kept up.

Sorting your home insurance isn’t just a tick-box exercise. In fact, you could even be losing money by paying for an insurance premium that won’t cover you. A broker, like Howden, can advise you on the best ways to tackle your home and contents insurance, and discuss your concerns in person, to give you clarity and peace of mind.

Find your nearest branch and speak to your local team.

Sources: BCIS, RebuildCostASSESSMENT, Bank of England inflation calculator